France E-Invoicing Reform

Are you ready for 1 September 2026?

Article written by Mélanie Lahoud

Partner Primexis / France

With less than 4 months to go before the first implementation date, the countdown to France’s e-invoicing reform has begun.

From 1 September 2026, all VAT-registered businesses in France must be able to receive electronic invoices through an Approved Platform. Depending on their size, some companies will also be required to issue electronic invoices from the same date.

In April 2025, we shared an initial overview of the reform in our article, Mandatory E-Invoicing & E-Reporting in France. As the go-live date approaches, companies should now move from awareness to action: selecting the right platform, reviewing invoice flows, assessing e-reporting obligations and preparing finance teams for new operational requirements.

If your business is VAT-registered in France and has not yet selected its Approved Platform, now is the time to act.

This reform is not only a technical change, it will impact invoice flows, VAT reporting, internal validation processes, ERP interfaces and accounting controls.

What is an Approved Platform (PA)? How to choose?

In France, the State will not provide a single platform for private-sector companies. VAT-registered businesses will need to rely on an Approved Platform, known in French as a Plateforme Agréée (PA), to receive and, where applicable, issue electronic invoices.

Companies are free to choose their Approved Platform. However, this choice should not be treated as a purely administrative decision. It should be assessed in light of the organisation’s needs, accounting model, ERP environment, invoice volumes, internal approval workflows and reporting obligations.

More than 100 platforms have already been approved by the French State. These platforms are responsible for issuing, transmitting and receiving electronic invoices, as well as extracting the information required by the tax authorities and transmitting transaction and payment data where relevant.

For companies that fully outsource their accounting to Primexis, our teams can propose selected providers’ solutions adapted to their organisation and operating model.

For companies using their own ERP or accounting software, the first step is to contact their software provider. This will help identify which Approved Platforms are compatible with existing systems and how to ensure smooth workflows, secure data exchange and optimised integration.

The list of platforms registered by the tax authorities is available here.

Who is impacted?

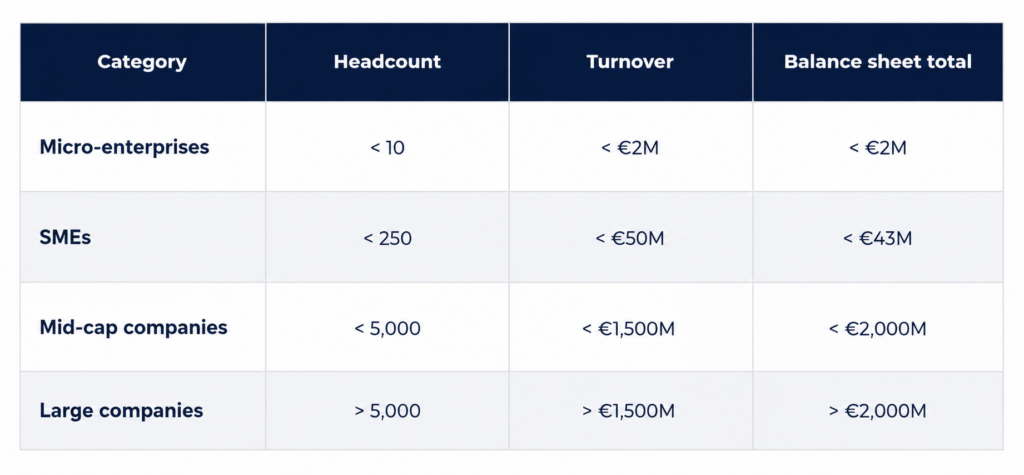

All entities subject to VAT in France are affected by the reform, including micro-enterprises, SMEs, mid-cap companies and large companies.

The implementation timeline depends on the size of the company. The table below summarises the main categories used to determine the applicable deadlines.

Specific attention for French branches

French branches of foreign companies registered for VAT in France should pay particular attention to the reform. Depending on their VAT position and transaction flows, they may be subject to specific e-invoicing and e-reporting obligations.

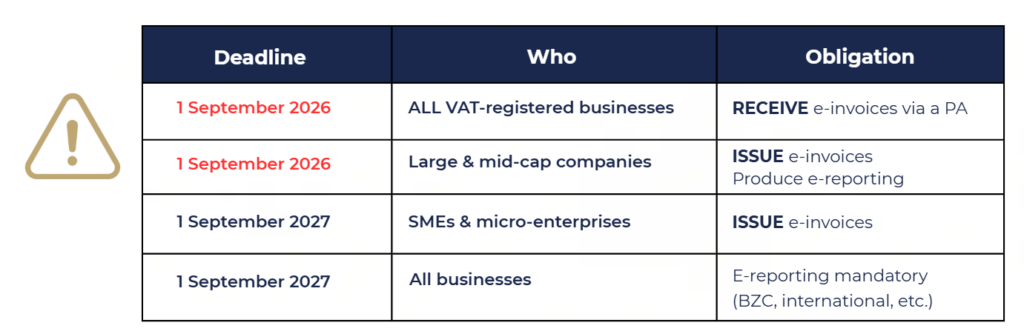

What are your key deadlines?

The reform will be implemented in phases. The first deadline, 1 September 2026, is critical for all VAT-registered businesses in France.

Although some companies have more time before they are required to issue e-invoices, the 2026 deadline remains essential for all VAT-registered businesses because the ability to receive electronic invoices will apply to everyone from the first phase.

E-reporting obligations will also apply according to the relevant scope of transactions, including certain B2C, international and other non-domestic flows.

What are your obligations?

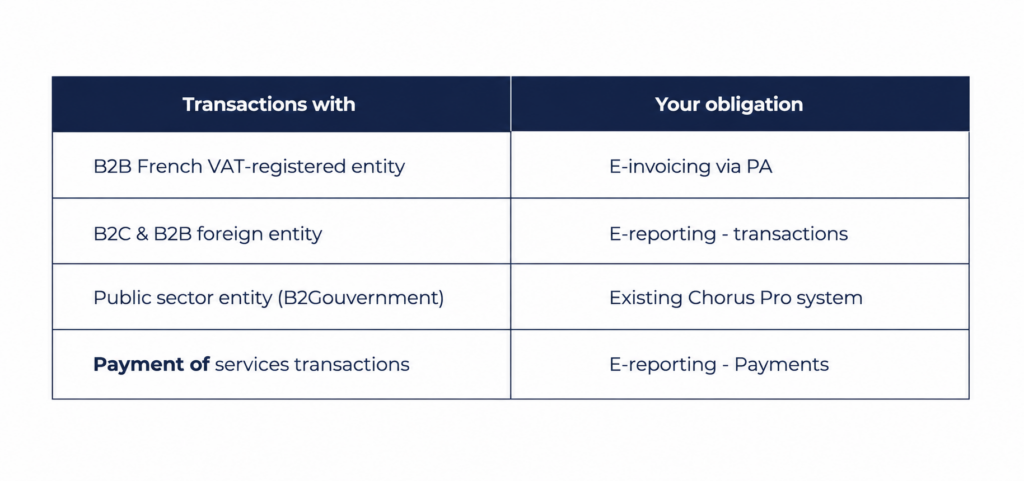

Your specific obligations depend on the type of counterparty you are transacting with and the nature of the transaction.

In practice, companies should distinguish between three key concepts:

- E-invoicing = Issuing and receiving structured electronic invoices, including formats such as Factur-X, UBL or CII

- E-reporting transactions = Reporting data for transactions that do not fall within the scope of domestic B2B e-invoicing, such as certain international, B2C or exempt transactions

- E- reporting payments = Reporting payment data for certain services transactions, particularly where VAT is due upon payment

It is important to note that e-invoicing is not only about using an Approved Platform to issue and receive invoices, it also involves managing validation workflows and updating invoice life cycle statuses within the platform.

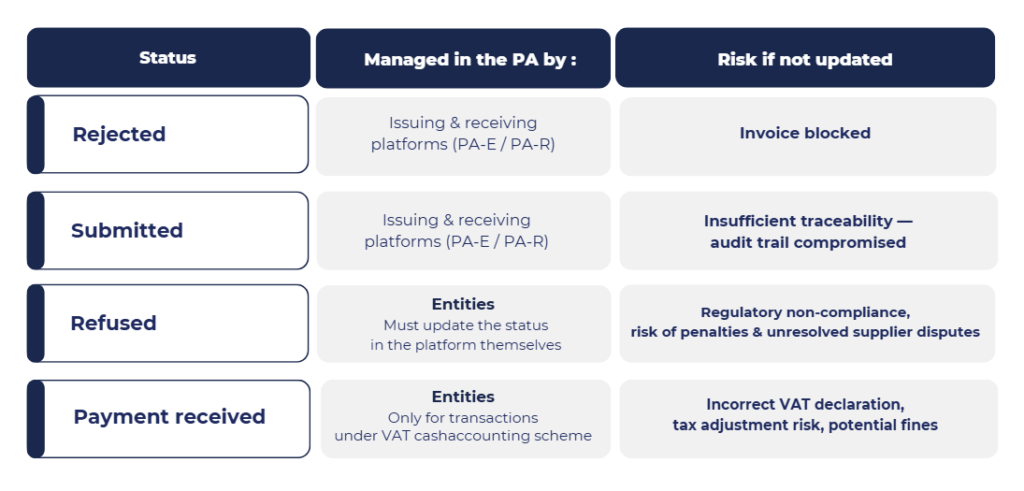

Life cycle statuses in the PA: who handles what?

E-invoicing is not just about using an approved platform to issue/receive invoices. It also involves managing validation workflows and updating invoice received statuses throughout their life cycle within the platform.

There are 4 life cycle statuses mentioned in the guidelines that need to be up to date in the PA:

- Statuses “Rejected” and “Submitted” are handled by the issuing and receiving platforms (PA-E and PA-R)

- Status “Refused” must be handled by the entities

- Status “Payment received” must be handled by the entities, but only for transactions subject to VAT under the cash accounting scheme (usually services transactions)

What are the risks of waiting?

Delaying preparation can create significant operational and financial consequences.

Key risks include:

- Inability to receive supplier invoices from September 2026

- Difficulties deducting input VAT if invoices are not compliant from the applicable mandatory date

- Financial penalties for non-compliant invoices or missing data transmissions

- Operational disruption and potential cash flow issues

- Increased manual work and data quality issues

- Loss of visibility over invoice statuses

- Missed opportunity to automate and streamline finance processes

Beyond penalties, the main risk is operational disruption. If platforms, systems, processes and teams are not ready, the transition may generate delays, manual reprocessing and loss of control over invoice flows.

Handled properly, the reform can also become a lever to improve invoice processing, strengthen internal controls, increase VAT data reliability and enhance visibility over supplier and customer flows.

How Primexis can help?

Whether your accounting is fully outsourced to Primexis or managed internally, our experts can support you at every stage of the reform.

Our International Business Services team works with French and international businesses to assess their obligations, secure their compliance roadmap and prepare their organisation for the transition to mandatory e-invoicing and e-reporting in France. Our objective is to help you secure the operational implementation of the reform while ensuring continuity in your accounting and VAT processes.

Compliance

- Identifying your obligations under the reform

- Proposing vetted solutions for outsourced accounting clients

- Designating your receiving Approved Platform & supporting registration processes where applicable

- Securing invoice receipt and issuance workflows

- Supporting invoice creation, archiving and follow-up

Advisory

- Mapping your current invoice flows and systems

- Reviewing your ERP and accounting tools as well as their compatibility with Approved Platforms;

- Selecting or reviewing an Approved Platform

- Analysing specific situations for French branches or international groups;

- Defining validation workflows and internal responsibilities

- Preparing internal procedures and documentation

- Training finance teams

Are you ready for 1 September 2026?

France’s mandatory e-invoicing and e-reporting reform is a major regulatory shift for all businesses operating in, or doing business with, France.

Contact our experts to discuss your situation and define the next steps for your organisation:

Mélanie LAHOUD

Partner – Corporate & Fund Services

melanie.lahoud@primexis.fr

Alexis GASTO

Partner – Head of Corporate & Fund Services

alexis.gasto@primexis.fr