Doing Business in France in 2026

What Foreign Investors Need to Know Before Entering the French Market

France remains one of Europe’s most attractive destinations for international companies looking to establish, expand or consolidate their presence in the European market. With access to the European Union single market, a highly skilled workforce, strong infrastructure, competitive R&D tax incentives and a robust legal framework, France offers foreign investors a powerful base for long-term growth.

However, doing business in France requires more than market ambition. International companies must understand local legal, accounting, tax, employment and payroll obligations before launching operations. Choosing the right structure, anticipating compliance requirements and working with experienced local advisors can make the difference between a smooth market entry and a complex, high-risk setup.

This overview highlights the key topics foreign investors should consider before doing business in France in 2026.

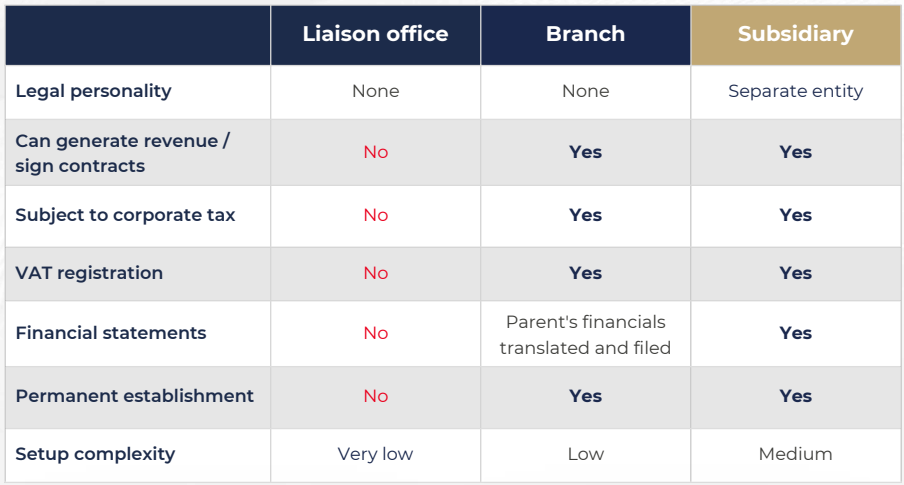

1. Choosing the right legal structure in France

One of the first decisions for a foreign company entering France is the choice of legal structure. This decision affects taxation, liability, governance, accounting obligations, employment setup and the overall credibility of the business in the French market.

Foreign investors generally compare three main options: a liaison office, a branch or a subsidiary.

- A liaison office is suitable for non-commercial activities such as market research, business development and initial exploration. It cannot generate revenue or sign commercial contracts. This structure may be useful for companies that want an initial presence in France before committing to full operations.

- A branch allows a foreign company to trade in France without creating a separate legal entity. It can generate revenue, sign contracts and register for VAT. However, because the branch is not legally separate from the parent company, the foreign parent remains directly liable for the French operations.

- A subsidiary is a French company incorporated under French law and controlled by a foreign parent. For many international groups, this is the preferred structure for a full implantation in France. It provides stronger liability protection, greater operational autonomy and stronger local credibility.

The SAS or SASU is often the most flexible and practical option for foreign subsidiaries in France, especially for international groups looking for adaptable governance and decision-making rules.

The right structure depends on the company’s commercial objectives, risk appetite, tax position, governance requirements and long-term plans in France.

2. Accounting and reporting obligations

Companies operating in France must keep accounts in accordance with French GAAP and the French Chart of Accounts. Bookkeeping must be performed transaction by transaction, in French and in euros. Each accounting entry must be supported by a source document, and accounting records must generally be retained for at least 10 years.

French companies must also prepare annual financial statements, usually including a balance sheet, income statement and notes to the financial statements. These statements must be approved by the annual general meeting and filed with the Commercial Court Registry.

Foreign groups should pay particular attention to the FEC, or Fichier des Écritures Comptables. This accounting file is required in a specific format in the event of a tax audit and must come directly from the accounting software.

For international groups, this is a key compliance point. Group reporting systems may not automatically produce a French-compliant FEC, especially when bookkeeping is initially maintained under group standards rather than French GAAP.

As a result, foreign companies should anticipate local accounting conversion, documentation and software requirements from the start.

3. Tax compliance in France

France has a comprehensive tax environment. Foreign investors must consider VAT, corporate income tax, withholding tax, local taxes, transfer pricing and specific tax declarations.

The standard VAT rate in France is 20%, although reduced rates may apply depending on the type of goods or services. Companies may be required to file VAT returns monthly, with quarterly filing possible in some cases.

Foreign companies with no permanent establishment in France must also pay close attention to VAT registration obligations. In some cases, the first taxable transaction in France may trigger a VAT registration requirement.

The standard corporate income tax rate in France is 25%. A reduced 15% rate may apply on profits up to a certain threshold, subject to conditions.

Foreign companies must also review other taxes and contributions, including withholding tax on dividends, the Social Solidarity Contribution known as C3S, and the Territorial Economic Contribution known as CET.

For international groups, transfer pricing is a major compliance and audit area. Transactions between related entities must be priced at arm’s length and documented appropriately.

Common risk areas include management fees, royalties, intragroup financing and year-end transfer pricing adjustments.

Tax compliance should therefore be considered early, not only at year-end. The French statutory accounts, group reporting, tax returns and transfer pricing documentation should be aligned from the beginning.

4. Preparing for French e-invoicing reform

France is introducing mandatory electronic invoicing and e-reporting obligations for VAT-registered businesses operating in France. The reform applies to B2B transactions and cross-border reporting, with invoices and data transmitted through certified platforms.

Large companies must begin issuing e-invoices from September 2026, while all companies must be able to receive e-invoices from September 2026. Mid-sized and small businesses will be required to issue e-invoices from September 2027.

Foreign groups operating in France should prepare early by reviewing their ERP, invoicing flows, master data, VAT processes and platform connectivity.

This reform is not only a technical invoicing project. It affects finance, tax, IT, data quality and internal processes.

Companies that prepare early will be better positioned to avoid disruption, reduce compliance risk and improve the reliability of their VAT reporting.

5. Hiring and payroll in France

France has one of the most protective employment frameworks in the world. This makes employment and payroll compliance a critical topic for foreign companies hiring in France. Employment contracts should be drafted carefully, usually with support from a specialist. The most common employment contract is the CDI, or permanent contract. Fixed-term contracts, known as CDDs, are permitted only in specific legal circumstances.

The applicable collective bargaining agreement is also essential in France. It sets sector-specific rules such as working hours, job classification, salary scales, probation periods and other employment conditions.

Foreign companies should identify the correct collective bargaining agreement before hiring their first employee.

Payroll in France is complex and highly regulated. Employer social contributions typically represent a significant additional cost on top of gross salary. Payroll must be processed monthly, payslips must be issued and the DSN, or Déclaration Sociale Nominative, must be submitted to French social security organisations from the first month of payroll.

Payroll compliance should therefore be operational before the first salary payment is made.

For foreign investors, this means employment contracts, payroll registration, benefits, social contributions, paid leave and reporting obligations must all be coordinated before hiring begins.

6. Scaling operations in France

As a company grows in France, new obligations may arise. A statutory auditor may be required when certain financial and employee thresholds are exceeded. Employee representation obligations also increase with headcount.

The Comité Social et Économique, or CSE, becomes mandatory from 11 employees, with its powers increasing as the company grows.

Profit-sharing becomes mandatory for companies with at least 50 employees for five consecutive years.

Other obligations may arise at different thresholds, including vocational training contributions, transport-related contributions, disability employment obligations, gender equality reporting and additional HR reporting.

Foreign investors should also consider R&D tax incentives such as the French R&D tax credit, or CIR. This regime can be highly valuable for innovation-driven companies, especially in technology, engineering, industrial, pharmaceutical and scientific sectors.

However, these incentives require robust documentation, technical evidence and coordination between finance, tax and operational teams.

Growth in France should therefore be anticipated from a compliance perspective. What is simple at the time of incorporation can become more complex as revenue, headcount and intragroup flows increase.

7. Common challenges for foreign investors

Foreign companies often underestimate the practical complexity of the French environment.

The most common challenges include choosing the right legal structure, aligning group reporting with French GAAP, producing a compliant FEC file, understanding VAT registration and e-invoicing obligations, managing corporate tax and withholding tax, documenting transfer pricing policies, setting up payroll from the first month, applying the correct collective bargaining agreement and monitoring employee representation thresholds.

These challenges are manageable with the right preparation and the right local partner. The key is to build a clear implementation roadmap before launching operations in France.

Legal, accounting, tax, payroll and HR decisions should not be treated separately. They are connected and can affect the cost, risk and efficiency of the French operation from day one.

How Primexis supports foreign investors in France

Primexis supports international groups and foreign investors at every stage of their French journey: incorporation, operations and maturity.

During the incorporation phase, Primexis can assist with domiciliation, registered address services, corporate secretary support, articles of association coordination and legal partner coordination.

During the operational phase, Primexis supports bookkeeping, management reporting, GAAP conversion, year-end closing, statutory financial statements, VAT, corporate tax returns, tax audit support, outsourced payroll and DSN filing.

As companies grow, Primexis can also support finance function transformation, management accounting, consolidation, reporting software implementation, outsourcing, secondment, transaction services, valuation services and fund services.

This combination of technical expertise and operational execution is particularly valuable for foreign companies that need to secure compliance while focusing on business growth.

For foreign investors, Primexis is more than a compliance provider. It is a trusted local partner for building, managing and scaling a business in France.

Preparing for a successful market entry in France

France offers strong opportunities for international companies, but successful market entry requires careful preparation. Legal structure, accounting setup, tax registration, VAT compliance, payroll processes and employment obligations should be anticipated before operations begin.

Foreign investors should also prepare for future growth by monitoring audit thresholds, headcount obligations, transfer pricing requirements, R&D tax incentives and upcoming e-invoicing obligations. A structured approach from day one helps reduce risk, improve compliance and support long-term growth in the French market.

Download the full 2026 guide to doing business in France

Planning to set up, expand or structure your operations in France?

Download the full Primexis “Doing Business in France 2026” guide to access a practical overview of the key legal, accounting, tax, VAT, payroll and employment obligations foreign investors need to know before entering the French market.