2026 Social Security Financing Act:

New Developments in Payroll & HR

While the 2026 Finance Act is still making its way through Parliament, the Social Security Financing Act (LFSS) has been permanently published. It introduces several major changes for Payroll and Human Resources departments, effective in 2026. Here is an overview of the main measures to remember.

Social Security Contributions: new measures and exemptions

Several important adjustments are to be expected in terms of social security contributions:

- Mutually agreed termination of contract and compulsory retirement

Employer contribution on the exempt portion of severance pay has increased from 30% to 40%, up to a limit of two annual Social Security caps (PASS), for all terminations taking effect on or after January 1, 2026.

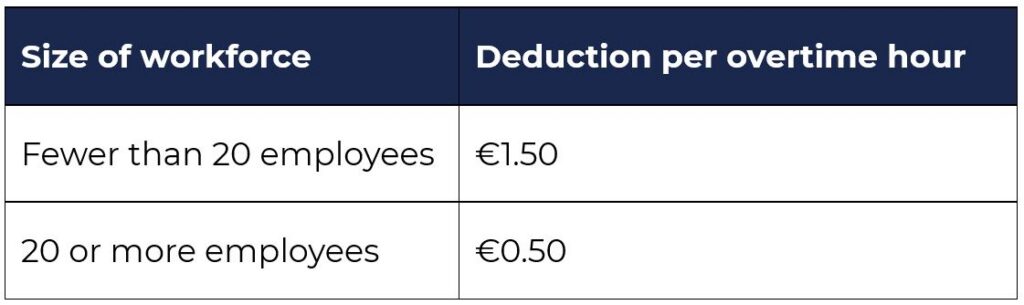

- Overtime

The employer’s flat-rate deduction has been extended to all companies, regardless of the size of their workforce.

⚠️ Please note, this does not apply to overtime hours worked by part-time employees.

Employment of Older Workers: strengthened measures

An “old age” penalty (malus) will be imposed on companies with 300 or more employees that fall to meet their obligation to negotiate on the employment of older workers. The specific terms and conditions will be set out in a future implementation decree.

New One-Time Decreasing General Reduction (RGDU)

The RGDU comes into force January 1, 2026. It replaces “illness” and “family allowance“ reductions up to 3x SMIC [French national minimum wage], with adaptations for certain sectors and schemes.

Two specific provisions are worth noting:

- Extended continuations of illness and family allowance reductions for certain special schemes.

- Adjusted calculation of the RGDU for companies whose minimum wages are less than the SMIC (€12.02 as of January 1, 2026): the reduction applies on the basis of the minimum wage and not the SMIC.

Work Stoppages: revisions to compensation conditions

The rules for compensating sick leave, occupational illnesses, and workplace accidents are undergoing significant change. This reform will impact both employers and employees, in particular in terms of duration and level of compensation.

Below is a summary of the main planned changes:

New Additional Birth Leave

A new additional birth leave has been established:

- Duration: up to 4 months, can be split.

- Compensation: compensated by national French Social Security (CPAM) at 70% and then 60% of net salary.

- Effective date: applicable July 1, 2026, for children born or adopted on or after January 1, 2026.

Additional Compensation: focus on management packages

The favorable social security regime applicable to management packages has been tightened to limit schemes that could be considered hidden salary.

From this point forward:

- Only gains that meet the conditions of the capital gains regime remain exempt.

- The 10% employee contribution has been revised.

- Social security contributions continue to apply.

⚠️ Please note, only arrangements involving a real economic risk benefit from favorable social security treatment. If not, the gains are treated as salary and subjected to contributions.

Employee Retirement: new measures

Several changes affect employee retirement.

Periods of maternity leave, adoption leave, or childcare leave are now counted as contribution periods for early retirement for those with “long careers.”

The rules on combining employment and retirement have been tightened with a refocusing on authorized activities and introduction of age limits.

Adjustments have been made to the “Macron” reform:

- Generations born between 1964 and 1968: gain of a few months.

- Generations born between 1964 and 1965: allocation of an additional quarter.

________________

Need assistance?

Do these changes affect you? Would you like to integrate these new developments into your HR processes or measure their operational impact?

Our Payroll & HR Consulting team is available to assist you:

📩 conseil.RH@primexis.fr

🌐 www.primexis.fr